9.4. Logistic Regression#

9.4.1. Why Not Linear Regression?#

Linear regression is a fundamental statistical technique that is widely used for modeling the relationship between a dependent variable and one or more independent variables. It has its strengths and weaknesses, and there are situations where it may not be suitable [James et al., 2023]:

Nonlinear Relationships: Linear regression assumes a linear relationship between the independent and dependent variables. If the true relationship is nonlinear, using linear regression can lead to poor model fit and inaccurate predictions.

Complex Interactions: Linear regression is limited in handling complex interactions between variables. If the relationship involves nonlinear effects, or higher-order terms, linear regression may not capture these nuances effectively.

Assumption Violations: Linear regression assumes that the residuals (the differences between observed and predicted values) are normally distributed and have constant variance. If these assumptions are violated, the results and inferences from linear regression may be unreliable.

Outliers and Influential Points: Linear regression is sensitive to outliers and influential data points. A single outlier can affect the regression line and the estimated coefficients.

Categorical and Binary Variables: While linear regression can handle continuous and numeric independent variables, it struggles with categorical or binary predictors without appropriate encoding or treatment.

Multi-Collinearity: When the independent variables in a linear regression model are highly correlated with each other, it can lead to multicollinearity issues. This makes it challenging to interpret the individual contributions of these variables.

Limited in Handling Non-Parametric Data: Linear regression is a parametric method, meaning it makes assumptions about the underlying data distribution. If the data is non-parametric or has heavy-tailed distributions, linear regression may not be appropriate.

In cases where these limitations are significant, other techniques such as nonlinear regression, generalized linear models, decision trees, support vector machines, neural networks, or other advanced statistical and machine learning methods may be more suitable. The choice of the appropriate modeling technique depends on the data.

9.4.2. Logistic Regression: Predicting a Binary Response Variable#

Logistic regression is a powerful statistical method tailored specifically for binary classification tasks. Its primary objective is to predict a binary response variable, such as yes/no or 0/1, by leveraging the impact of one or more predictor variables. This approach is effectively represented by the logistic regression model [James et al., 2023].

9.4.2.1. Logistic Model#

At the core of logistic regression is its ingenious model, which seamlessly integrates predictor variables within a linear framework, further molded by the logistic function. This fusion aims to predict the probability of the positive class (class 1) in a binary response scenario. The model is encapsulated by the following equation [James et al., 2023]:

In this equation:

\(X = (X_1, ..., X_p)\) constitutes the vector of predictor variables (features).

\(\beta_0, \beta_1, ..., \beta_p\) take on the roles of coefficients, encompassing both the intercept and each predictor variable’s contribution.

\(p(X)\) designates the probability of the positive class, informed by the predictor variables.

Notably, the term \(\log[p(X)/[1 - p(X)]]\), dubbed the log-odds, encapsulates the relationship between the probability of positive and negative outcomes [James et al., 2023]. The odds ratio, which is the exponentiated value of the log-odds, represents the ratio of the odds of the positive class to the odds of the negative class.

9.4.2.2. Estimating Probabilities#

The logistic model allows us to deduce the estimated probability of the positive class given the predictor variables (\(p(X)\)) through the following equation:

In this equation, the exponential function (approximately 2.71828) plays a pivotal role in the transformation. This transformation, facilitated by the logistic function, also known as the sigmoid function, molds the linear combination of predictor variables into a probability value that spans the entire spectrum between 0 and 1.

9.4.2.3. Sigmoid (Logistic) Function#

The equation given below:

is closely connected to the sigmoid (logistic) function within the context of logistic regression, a method used for binary classification.

In logistic regression, the objective is to estimate the likelihood of the positive outcome (class 1) based on the values of certain predictor variables, such as \(X_1, X_2, \ldots, X_p\). The left side of the equation, \(\ln\left(\frac{p(X)}{1 - p(X)}\right)\), signifies the log-odds (logit) of the probability of the positive outcome given the predictor variables. This transformation linearizes the connection between the predictor variables and the probability.

Now, let’s introduce the sigmoid function. The sigmoid function, denoted as \(f(x) = \dfrac{1}{1 + e^{-x}}\), converts a real-number \(x\) into a probability ranging from 0 to 1. In the logistic regression model, this can be related to \(p(X)\) as follows:

In this expression, \(p(X)\) represents the probability of the positive outcome. The right-hand side is a linear combination of predictor variables, each multiplied by coefficients \(\beta_0, \beta_1, \ldots, \beta_p\). The sigmoid function, also known as the logistic function, is applied to this combination, ensuring that the result, \(p(X)\), remains within the range of 0 to 1.

In essence, the logistic regression model incorporates the sigmoid function to transform the linear combination of predictor variables into a valid probability value, enabling binary classification decisions based on this probability threshold.

Note

scipy.special.expit is a function within the SciPy library, a widely recognized open-source resource for scientific and mathematical computations. This function, also known as the “exponential of the logistic function,” serves the purpose of executing a logistic sigmoid transformation. It operates on either a single value or an array as input and employs the logistic sigmoid function, mathematically expressed as:

Here, \(e\) signifies the natural logarithm base, while \(x\) denotes the input variable. The fundamental role of the logistic sigmoid function is to transform input values into a bounded range of 0 to 1. This property finds extensive application in various domains, including machine learning, specifically in logistic regression, where it is instrumental in modeling the probability of binary outcomes.

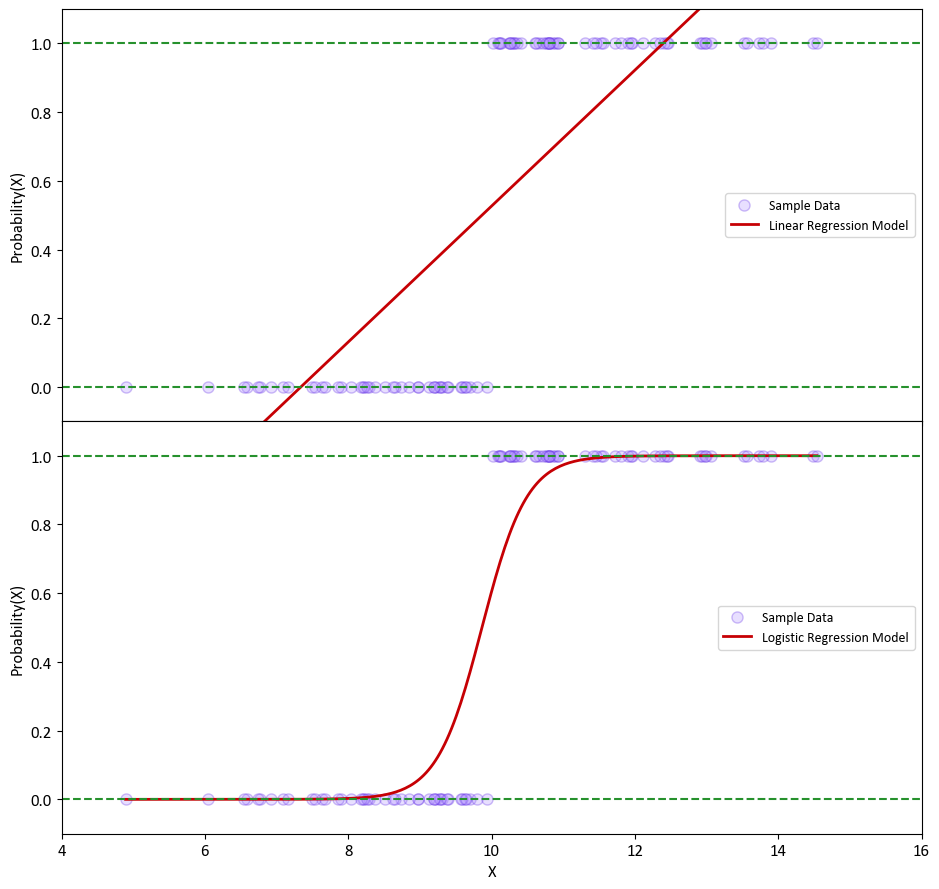

Example: Let’s examine a straightforward scenario with a single variable, denoted as X, and a dependent variable, y. In this instance, we generate X values from a normal distribution with a mean (\(\mu\)) of 10 and a standard deviation (\(\sigma\)) of 2. The variable y is defined as follows:

Next, we estimate the probability of the outcome using linear regression, which is depicted in the top plot. It’s worth noting that some of the estimated probabilities turn out to be negative, which is problematic because probabilities should always fall within the range of 0 to 1.

To address this issue, we employ logistic regression, as shown in the bottom plot. In logistic regression, all estimated probabilities strictly conform to the valid probability range, ensuring that they stay between 0 and 1.

import matplotlib.pyplot as plt

plt.style.use('../mystyle.mplstyle')

import numpy as np

# from scipy.special import expit

from sklearn.linear_model import LinearRegression, LogisticRegression

mu, sigma = 10, 2 # mean and standard deviation

np.random.seed(0)

X = np.random.normal(mu, sigma, 100)

y = np.where(X > mu, 1, 0)

X = X.reshape(-1, 1)

X_gen = np.linspace(X.min(), X.max(), 300)

# Create the models

models = [LinearRegression(), LogisticRegression()]

# Titles for the plots

titles = [ "Linear Regression Model", "Logistic Regression Model"]

fig, axes = plt.subplots(2, 1, figsize=(9.5, 9), sharex=True, gridspec_kw={'hspace': 0})

for i, ax in enumerate(axes):

model = models[i]

model.fit(X, y)

if i == 1:

Px = (1/(1 + np.exp(- (X_gen * model.coef_ + model.intercept_)))).flatten()

# Or we could utilize scipy.special.expit

# Px = expit(X_gen * model.coef_ + model.intercept_).ravel()

else:

Px = model.coef_ * X_gen + model.intercept_

ax.scatter(X, y, color='#b496ff', ec='#602ce5', alpha=0.3, label="Sample Data")

ax.plot(X_gen, Px, color='#C60004', lw=2, label=titles[i])

ax.set_xlim([4, 16])

ax.hlines([0, 1], *ax.get_xlim(), linestyles='dashed', color = '#26912d', lw=1.5)

ax.set(xlabel='' if i == 0 else 'X', ylabel='Probability(X)')

ax.grid(False)

ax.legend(loc = 'right')

ax.set_ylim(-0.1, 1.1)

plt.tight_layout()

Remark

Logistic regression is primarily used for classification, not regression, despite its name. It’s a statistical model used to predict the probability of a binary outcome, typically denoted as class 0 and class 1. The logistic regression model estimates the probability that a given input belongs to one of these two classes. This makes it a valuable tool for various classification tasks, such as spam detection, disease diagnosis, or sentiment analysis. In logistic regression, the output is a probability score, and a threshold (often 0.5) is applied to classify the input into one of the two classes. Therefore, it’s fundamentally a classification technique, even though the term “regression” is in its name.

9.4.2.4. Finding the Coefficients#

In logistic regression, the goal is to find the optimal coefficients (\(\beta_0\), \(\beta_1\), …, \(\beta_p\)) of the model that best fits the data. This is achieved through the Maximum Likelihood Estimation (MLE) method. MLE aims to determine the coefficient values that maximize the likelihood of observing the actual binary outcomes in the dataset, given the predictor variables:

Formulate the Likelihood Function: Begin by defining the likelihood function, denoted as \(L(\beta_0, \beta_1, ..., \beta_p)\), which represents the probability of observing the binary outcomes (0s and 1s) based on the logistic regression model. This function is a mathematical representation of the relationship between the coefficients and the observed data.

Take the Natural Logarithm: Simplify the likelihood calculations by working with the natural logarithm of the likelihood function, denoted as \(\ell(\beta_0, \beta_1, ..., \beta_p)\). This transformation preserves the underlying structure while making computations more manageable.

Maximize the Log-Likelihood: Utilize optimization techniques, often numerical methods, to find the coefficient values that maximize the log-likelihood function \(\ell(\beta_0, \beta_1, ..., \beta_p)\). The goal is to identify the coefficient values that make the observed data most likely under the logistic regression model.

Interpret the Coefficients: Once the estimated coefficients \(\hat{\beta}_0, \hat{\beta}_1, ..., \hat{\beta}_p\) are obtained, interpret their values. Each coefficient (excluding \(\hat{\beta}_0\), the intercept) represents the change in the log-odds (logit) of the positive outcome (class 1) associated with a one-unit change in the corresponding predictor variable while holding other variables constant.

Practical implementations of logistic regression, especially with multiple predictor variables (\(X_1\), \(X_2\), …, \(X_p\)) and non-linear optimization, can be complex. The choice of optimization method may depend on the software libraries or statistical packages you are using.

Most modern statistical software packages for data analysis, such as Python’s scikit-learn or R’s glm function, provide built-in functions to perform logistic regression. These functions automatically handle the MLE process and provide the estimated coefficients. However, if manual implementation of logistic regression is necessary, you’ll likely rely on optimization algorithms like gradient descent or more advanced techniques. Proficiency in numerical optimization and statistical concepts is crucial for successfully implementing this process from scratch.

Remark

Maximum Likelihood Estimation (MLE) is a statistical method used to estimate the parameters of a statistical model. The goal of MLE is to find the parameter values that make the observed data most probable under the assumed probabilistic model. This technique is widely used in various fields, including statistics, econometrics, machine learning, and many other areas where data analysis and modeling are essential.

Likelihood Function: The likelihood function, denoted as \(L(\theta)\), is a fundamental concept in MLE. It represents the probability of observing the given data points, assuming a specific parametric model. For a continuous distribution, the likelihood is a function of the parameters of that distribution.

Parameter Estimation: In many statistical models, there are parameters (denoted as \(\theta\)) that need to be estimated from the data. The likelihood function is a function of these parameters. The MLE method seeks the values of these parameters that maximize the likelihood function.

Log-Likelihood: To simplify calculations and numerical stability, it’s common to work with the natural logarithm of the likelihood function, denoted as \(\ell(\theta)\). Maximizing the log-likelihood is equivalent to maximizing the likelihood itself, as the logarithm is a monotonically increasing function.

Optimization: Finding the values of the parameters that maximize the log-likelihood function \(\ell(\theta)\) is an optimization problem. Various optimization algorithms, such as gradient descent, Newton-Raphson, or more advanced techniques, can be employed to search for the optimal parameter values.

Statistical Inference: Once the MLE estimates of the parameters, denoted as \(\hat{\theta}\), are obtained, they can be used for statistical inference. This includes making predictions, calculating confidence intervals, performing hypothesis tests, and evaluating the goodness of fit of the model to the data.

MLE is a powerful and widely used method because it provides estimates that are asymptotically unbiased and efficient under certain conditions. However, it’s essential to ensure that the chosen model is appropriate for the data, as MLE can be sensitive to model misspecification. Additionally, for complex models, numerical optimization may be computationally intensive, and care must be taken to handle issues like local optima.

9.4.2.5. Translating Theory into Python#

In the world of Python, the practical implementation of logistic regression is greatly simplified by leveraging powerful libraries like scikit-learn. This Python library provides a comprehensive toolkit for machine learning, and the LogisticRegression class from scikit-learn is an invaluable tool for binary classification tasks. By utilizing this class, you can effortlessly apply logistic regression to your dataset, allowing you to fit the model and gain access to the estimated coefficients.

For those eager to explore the depths of logistic regression within the scikit-learn ecosystem, the official scikit-learn documentation for the LogisticRegression class serves as a valuable resource. It acts as a gateway to the LogisticRegression class, providing detailed insights and instructions on how to utilize it effectively: scikit-learn Logistic Regression Documentation. This documentation is an essential reference for both beginners and experienced practitioners, offering guidance on various parameters, techniques, and best practices for applying logistic regression in diverse real-world scenarios.

Example: In the next example, we turn our attention to the utilization of the Default dataset from the ISLR repository [James et al., 2023]. This dataset, available at (https://www.statlearning.com/resources-python). This dataset encapsulates a comprehensive record of instances where customers defaulted on their credit obligations.

import pandas as pd

Default = pd.read_csv('Default.csv')

Default.columns = [x.title() for x in Default.columns]

display(Default.head(5))

| Default | Student | Balance | Income | |

|---|---|---|---|---|

| 0 | No | No | 729.526495 | 44361.625074 |

| 1 | No | Yes | 817.180407 | 12106.134700 |

| 2 | No | No | 1073.549164 | 31767.138947 |

| 3 | No | No | 529.250605 | 35704.493935 |

| 4 | No | No | 785.655883 | 38463.495879 |

Note

In the context of credit cards, “default” refers to the failure of a cardholder to meet the agreed-upon terms and obligations associated with the credit card account. This typically includes missing minimum monthly payments, exceeding the credit limit, or violating other terms specified in the credit card agreement. When a cardholder defaults, it indicates a breach of the contract between the cardholder and the credit card issuer.

import warnings

warnings.simplefilter(action='ignore', category=FutureWarning)

import matplotlib.pyplot as plt

import seaborn as sns

plt.style.use('../mystyle.mplstyle')

fig, ax = plt.subplots(1, 3, figsize=(9.5, 4.5), gridspec_kw = {'width_ratios':[.6,.2,.2]})

CP = {'Yes': 'MediumSeaGreen', 'No': 'OrangeRed'}

# Left

_ = ax[0].scatter(Default.loc[Default.Default == 'Yes', 'Balance'],

Default.loc[Default.Default == 'Yes', 'Income'],

edgecolors=CP['Yes'], label='Yes')

_ = ax[0].scatter(Default.loc[Default.Default == 'No', 'Balance'],

Default.loc[Default.Default == 'No', 'Income'],

edgecolors=CP['No'], label='No', alpha=0.2)

_ = ax[0].set_ylim([0, 8e4])

_ = ax[0].set(xlabel='Balance', ylabel='Income')

_ = ax[0].legend(title='Default', loc='upper right')

# Center

_ = sns.boxplot(x='Default', y='Balance', data=Default, orient='v', ax=ax[1], palette=CP)

_ = ax[1].set_ylim([-100, 3e3])

# Right

_ = sns.boxplot(x='Default', y='Income', data=Default, orient='v', ax=ax[2], palette=CP)

_ = ax[2].set_ylim([-100, 8e4])

plt.tight_layout()

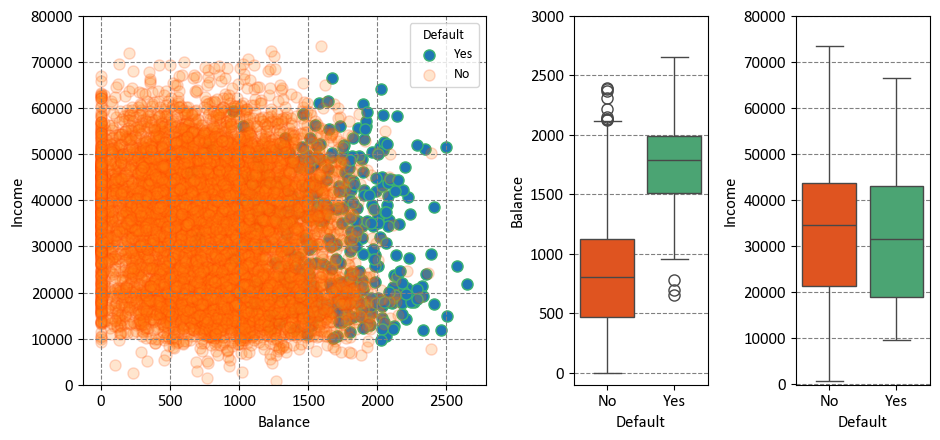

The Default dataset is portrayed through three enlightening panels. Let’s explore each [James et al., 2023]:

Left Panel: Within this panel, the yearly incomes and monthly credit card balances of diverse individuals are visually depicted. Individuals who encountered default in their credit card payments are distinctly portrayed in Orange, while those who successfully averted default are prominently showcased in Green. This visualization immediately illuminates the dynamic interplay between income, credit card balance, and credit card payment outcomes.

Center Panel: At the heart of this panel, a series of boxplots takes prominence, providing insights into the distribution of credit card balances in relation to default status. These boxplots offer a comprehensive overview of medians, quartiles, and potential outliers within each default group. The contrast between individuals who experienced default and those who did not is vividly delineated, succinctly revealing disparities in balances.

Right Panel: Complementing the center panel, the right panel introduces a pair of boxplots that cast a spotlight on income variation according to default status. These boxplots concisely capture nuanced shifts in income distribution for both defaulters and non-defaulters, offering a visual narrative that illuminates the role income plays in credit card payment outcomes.

The Student status can be effectively represented using a dummy variable, which is a common technique in data analysis and machine learning. This involves creating a binary variable that takes the value of 1 if the individual is a student, and 0 if the individual is not a student. In mathematical terms, this encoding can be expressed as:

In this context:

When an individual’s Student status is true, the corresponding value of the dummy variable is set to 1, indicating that the individual is a student.

Conversely, if an individual is not a student, the dummy variable takes the value of 0, signifying the non-student status.

This approach simplifies the representation of Student status in a format that can be effectively utilized in various analyses and predictive modeling scenarios. It provides a straightforward and standardized way to incorporate categorical information like Student status into computational workflows.

df = Default.copy()

df['Default'], _ = Default.Default.factorize()

df['Student'], _ = Default.Student.factorize()

print('From:')

display(Default.head(5))

print('To')

display(df.head(5))

From:

| Default | Student | Balance | Income | |

|---|---|---|---|---|

| 0 | No | No | 729.526495 | 44361.625074 |

| 1 | No | Yes | 817.180407 | 12106.134700 |

| 2 | No | No | 1073.549164 | 31767.138947 |

| 3 | No | No | 529.250605 | 35704.493935 |

| 4 | No | No | 785.655883 | 38463.495879 |

To

| Default | Student | Balance | Income | |

|---|---|---|---|---|

| 0 | 0 | 0 | 729.526495 | 44361.625074 |

| 1 | 0 | 1 | 817.180407 | 12106.134700 |

| 2 | 0 | 0 | 1073.549164 | 31767.138947 |

| 3 | 0 | 0 | 529.250605 | 35704.493935 |

| 4 | 0 | 0 | 785.655883 | 38463.495879 |

Note

A dummy variable, often referred to as an indicator or binary variable, is a fundamental concept in the realm of statistics and econometrics. It essentially serves as a numerical representation of categorical data or group membership by adopting either of two values, which are typically 0 or 1. The primary purpose of dummy variables is to provide a means to incorporate categorical information into quantitative analyses. The key aspects of dummy variables can be elucidated as follows:

Representation of Categorical Data: Dummy variables find utility in symbolizing categories or distinct levels within a categorical variable. For instance, if we consider a categorical variable like “Color” encompassing values such as “Red,” “Green,” and “Blue,” we can create three corresponding dummy variables. These dummy variables take on values of 0 or 1 to indicate whether a particular observation belongs to a given category.

Binary Coding Approach: The encoding of dummy variables follows a binary convention. In the context of a categorical variable featuring “k” categories, “k-1” dummy variables are generated. Each individual dummy variable is associated with a specific category, with a value of 1 denoting that an observation pertains to that category, while a value of 0 signifies that it does not. This practice is adopted to prevent multicollinearity, which arises when including all “k” dummy variables could lead to interdependencies.

Utilization in Regression Analysis: Dummy variables play a prevalent role in regression analysis, particularly within the domain of multiple regression. They facilitate the integration of categorical variables into regression models, permitting the assessment of the influence of different categories on the dependent variable. Through the incorporation of dummy variables, one can delineate the effects of each category independently.

Illustrative Scenario: As an illustration, consider an investigation into the impact of education levels on income. A categorical variable representing education may include categories such as “High School,” “Bachelor’s,” and “Master’s.” In this context, two dummy variables would be fashioned—one for “Bachelor’s” and one for “Master’s.” If an individual possesses a Bachelor’s degree, the “Bachelor’s” dummy variable assumes a value of 1, while the “Master’s” dummy variable retains a value of 0. Conversely, if an individual holds a Master’s degree, the “Master’s” dummy variable would be 1, and the “Bachelor’s” dummy variable would be 0.

Dummy variables serve as a fundamental tool for translating categorical data into a format amenable to quantitative analysis. Their application is pervasive, particularly in the realm of statistical modeling, where they are harnessed extensively in regression analyses to accommodate categorical variables and investigate their impact on other variables of interest.

Remark

The pandas.factorize() function is a useful tool in the pandas library for converting categorical data into numerical representations. It assigns a unique integer to each unique category (factor) in the input array, which makes it easier to work with categorical data in numerical computations and machine learning algorithms:

import pandas as pd

# Sample categorical data

data = ['apple', 'banana', 'apple', 'banana', 'apple', 'orange']

# Using pandas.factorize() to convert categorical data to numerical labels

labels, uniques = pd.factorize(data)

print("Original Data:", data)

print("Encoded Labels:", labels)

print("Unique Categories:", uniques)

Output:

Original Data: ['apple', 'banana', 'apple', 'banana', 'apple', 'orange']

Encoded Labels: [0 1 0 1 0 2]

Unique Categories: Index(['apple', 'banana', 'orange'], dtype='object')

In the example above, the pandas.factorize() function converts the categorical data (‘apple’, ‘banana’, ‘apple’, ‘banana’, ‘apple’, ‘orange’) into numerical labels (0, 1, 0, 1, 0, 2), and it also returns the unique categories as an index object.

9.4.3. Simple Logistic Regression#

Let’s explore a logistic regression approach characterized by the following equation:

This formulation encapsulates the likelihood of default occurrence. It revolves around the effect of the ‘Balance’ predictor. While we initially mentioned ‘Student’ status and ‘Income’ as contributors, for clarity, we’ll focus on ‘Balance’ in this representation.

The probability of default, denoted as \( p(X) \), is expressed as follows:

Breaking down the elements of the equation:

\( \beta_0 \) and \( \beta_1 \) are coefficients associated with the intercept and ‘Balance’, respectively.

‘Balance’ serves as the predictor variable that shapes the logistic regression model’s outcome.

The natural logarithm (\( \log \)) is applied to the odds ratio \( \frac{p(X)}{1 - p(X)} \), enabling the representation of the relationship between the ‘Balance’ predictor and the log-odds of default in a linear manner.

The exponentiation (\( e^{\dots} \)) incorporated within the formula translates the log-odds into a probability scale.

In essence, this logistic regression equation dissects the impact of ‘Balance’ on predicting the probability of default, providing a focused lens into this specific predictor’s role in the model.

Within the context of the Default dataset, logistic regression serves as a potent tool for modeling the probability of encountering default. To illustrate, consider the probability of default given a specific balance, which can be expressed as:

In this formulation, logistic regression enables us to quantitatively assess the likelihood of a default occurrence based on the observed balance value. This probability-based perspective provides valuable insights into the potential outcomes within the dataset, shedding light on the dynamics between credit card balances and the probability of encountering default.

import numpy as np

from sklearn.linear_model import LogisticRegression

X = df['Balance'].values.reshape(-1, 1)

y = df['Default'].values

# Generating test data

X_gen = np.arange(X.min(), X.max()).reshape(-1, 1)

log_reg = LogisticRegression()

_ = log_reg.fit(X, y)

Pred_proba = log_reg.predict_proba(X_gen)

Remark

Conditional probability is a fundamental concept in probability theory that deals with the likelihood of an event occurring given that another event has already occurred. In other words, it quantifies the probability of an event happening under a specific condition or constraint.

Mathematically, the conditional probability of event A occurring given event B has occurred is denoted as P(A|B) and is calculated as:

Where:

\( P(A|B) \) is the conditional probability of event A given event B.

\( P(A \cap B) \) is the probability that both events A and B occur.

\( P(B) \) is the probability of event B occurring.

Key points to remember about conditional probability:

The denominator, \( P(B) \), ensures that we are considering only the subset of situations in which event B has occurred.

If events A and B are independent, then \( P(A|B) = P(A) \), meaning that the occurrence of event B has no impact on the probability of event A.

Conditional probability is essential for understanding real-world situations where outcomes are influenced by certain conditions. For instance, in medical diagnosis, the probability of having a disease may change based on the results of specific tests.

The concept of conditional probability forms the basis for Bayes’ theorem, a powerful tool for updating probabilities based on new evidence.

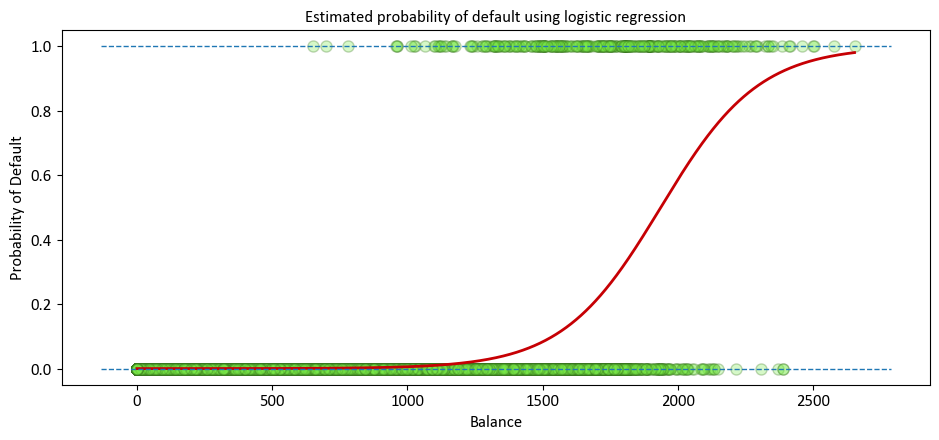

fig, ax = plt.subplots(1, 1, figsize=(9.5, 4.5))

_ = ax.scatter(X, y, color='#7aea49', ec = '#38761d', alpha = 0.3)

_ = ax.plot(X_gen, Pred_proba[:, 1], color='#C60004', lw=2)

_ = ax.hlines([0, 1], *ax.get_xlim(), linestyles='dashed', lw=1)

_ = ax.set(xlabel = 'Balance', ylabel='Probability of Default',

title = 'Estimated probability of default using logistic regression')

_ = ax.grid(False)

plt.tight_layout()

The predicted probabilities of default are showcased, derived from the logistic regression method. Unlike the left panel, these probabilities align with the fundamental concept of probability, always lying within the range of 0 to 1. This adherence to the proper probability range is a distinctive trait of logistic regression’s predictions.

An alternative approach is to utilize the Statsmodels Generalized Linear Models library.

import statsmodels.api as sm

import statsmodels.formula.api as smf

# Also recall our Reg_Result for OLS Reression results

def Reg_Result(Inp):

Temp = pd.read_html(Inp.summary().tables[1].as_html(), header=0, index_col=0)[0]

display(Temp.style\

.format({'coef': '{:.4e}', 'P>|t|': '{:.4e}', 'std err': '{:.4e}'})\

.bar(subset=['coef'], align='mid', color='Lime')\

.set_properties(subset=['std err'], **{'background-color': 'DimGray', 'color': 'White'}))

model = smf.glm(formula = 'Default ~ Balance', data = df, family=sm.families.Binomial())

Results = model.fit()

print(Results.summary())

Reg_Result(Results)

Generalized Linear Model Regression Results

==============================================================================

Dep. Variable: Default No. Observations: 10000

Model: GLM Df Residuals: 9998

Model Family: Binomial Df Model: 1

Link Function: Logit Scale: 1.0000

Method: IRLS Log-Likelihood: -798.23

Date: Sat, 27 Jan 2024 Deviance: 1596.5

Time: 23:46:35 Pearson chi2: 7.15e+03

No. Iterations: 9 Pseudo R-squ. (CS): 0.1240

Covariance Type: nonrobust

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

Intercept -10.6513 0.361 -29.491 0.000 -11.359 -9.943

Balance 0.0055 0.000 24.952 0.000 0.005 0.006

==============================================================================

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | -1.0651e+01 | 3.6100e-01 | -29.491000 | 0.000000 | -11.359000 | -9.943000 |

| Balance | 5.5000e-03 | 0.0000e+00 | 24.952000 | 0.000000 | 0.005000 | 0.006000 |

In particular, for

model = smf.glm(formula='Default ~ Balance', data=df, family=sm.families.Binomial())

we have,

formula='Default ~ Balance': This is the formula notation used to specify the relationship between the response variable (‘Default’) and the predictor variable (‘Balance’). The tilde symbol (~) separates the response variable from the predictor variable. In this case, it signifies that we are modeling the influence of ‘Balance’ on the likelihood of ‘Default’.family=sm.families.Binomial(): This parameter defines the error distribution or family of the model. In this case, we’re using the Binomial distribution, which is appropriate for binary response variables. Thesm.families.Binomial()indicates that we’re using the Binomial distribution from the Statsmodels library.

9.4.4. Multiple Logistic Regression#

Let’s delve into an alternative logistic regression approach characterized by the following equation:

This formulation encapsulates the likelihood of encountering default. It hinges on the contribution of multiple predictors, including ‘Student’ status, ‘Balance’, and ‘Income’. The probability of default, \( p(X) \), is expressed as follows:

In this equation:

\( \beta_0 \), \( \beta_1 \), \( \beta_2 \), and \( \beta_3 \) are the coefficients corresponding to the intercept, ‘Student’ status, ‘Balance’, and ‘Income’, respectively.

‘Student’, ‘Balance’, and ‘Income’ are the predictor variables that contribute to the logistic regression model.

The natural logarithm (\( \log \)) is applied to the odds ratio \( \frac{p(X)}{1 - p(X)} \) to linearly model the relationship between the predictors and the log-odds of default.

The exponentiation (\( e^{\dots} \)) within the formula facilitates the transformation of the log-odds back to the probability scale.

In essence, this logistic regression equation accounts for the combined influence of ‘Student’ status, ‘Balance’, and ‘Income’ in predicting the probability of default.

An alternative approach is to utilize the Statsmodels Generalized Linear Models library.

formula = 'Default ~ Student + Income + Balance'

model = smf.glm(formula = formula, data=df, family=sm.families.Binomial())

Results = model.fit()

print(Results.summary())

Reg_Result(Results)

Generalized Linear Model Regression Results

==============================================================================

Dep. Variable: Default No. Observations: 10000

Model: GLM Df Residuals: 9996

Model Family: Binomial Df Model: 3

Link Function: Logit Scale: 1.0000

Method: IRLS Log-Likelihood: -785.77

Date: Sat, 27 Jan 2024 Deviance: 1571.5

Time: 23:46:35 Pearson chi2: 7.00e+03

No. Iterations: 9 Pseudo R-squ. (CS): 0.1262

Covariance Type: nonrobust

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

Intercept -10.8690 0.492 -22.079 0.000 -11.834 -9.904

Student -0.6468 0.236 -2.738 0.006 -1.110 -0.184

Income 3.033e-06 8.2e-06 0.370 0.712 -1.3e-05 1.91e-05

Balance 0.0057 0.000 24.737 0.000 0.005 0.006

==============================================================================

| coef | std err | z | P>|z| | [0.025 | 0.975] | |

|---|---|---|---|---|---|---|

| Intercept | -1.0869e+01 | 4.9200e-01 | -22.079000 | 0.000000 | -11.834000 | -9.904000 |

| Student | -6.4680e-01 | 2.3600e-01 | -2.738000 | 0.006000 | -1.110000 | -0.184000 |

| Income | 3.0330e-06 | 8.2000e-06 | 0.370000 | 0.712000 | -0.000013 | 0.000019 |

| Balance | 5.7000e-03 | 0.0000e+00 | 24.737000 | 0.000000 | 0.005000 | 0.006000 |

As an illustration for the recent model, let’s take the case of two individuals: James, a student, and Robert, a non-student. Both individuals possess a credit card balance of $1,200 and an income of $40,000. We can now examine the estimated probabilities of default for these two individuals:

df0=pd.DataFrame({'Student':[1,0],'Income':[40,40],'Balance':[1500,1500]},index=['James', 'Robert'])

display(df0)

| Student | Income | Balance | |

|---|---|---|---|

| James | 1 | 40 | 1500 |

| Robert | 0 | 40 | 1500 |

E=np.exp(Results.params['Intercept']+Results.params['Student']*df0['Student']\

+Results.params['Income']*df0['Income']+Results.params['Balance']*df0['Balance'])

P=E/(1+E)

pd.DataFrame(P,columns=['Probability of defaults'])

| Probability of defaults | |

|---|---|

| James | 0.051615 |

| Robert | 0.094135 |

This observation highlights that students generally exhibit higher probabilities of default compared to non-students.

9.4.5. Confounding (Optional Content)#

Confounding in statistics refers to a situation where the relationship between two variables is distorted or influenced by the presence of a third variable, known as a confounder or a confounding variable. This confounder is related to both the independent and dependent variables, creating a scenario where the observed association between the independent and dependent variables might be misleading or inaccurate [James et al., 2023].

Confounding variables can introduce bias and lead to incorrect conclusions when analyzing the relationship between variables. To address confounding, researchers need to carefully control or adjust for the effects of confounding variables in their analyses. This can be achieved through techniques like stratification, matching, or statistical modeling, such as multiple regression.

In essence, confounding occurs when the observed relationship between two variables is not a true causal relationship but is influenced by the presence of a third variable that affects both variables being studied. Identifying and accounting for confounding is crucial to ensuring accurate and reliable statistical analyses and interpretations.

from sklearn.linear_model import LogisticRegression

# Non-Students

# Extracting data for non-students

X_NotStudent = df.loc[df.Student == 0, 'Balance'].values.reshape(-1, 1)

y_NotStudent = df.loc[df.Student == 0, 'Default']

# Creating a logistic regression model for non-students

log_reg_NotStudent = LogisticRegression(solver='newton-cg')

_ = log_reg_NotStudent.fit(X_NotStudent, y_NotStudent)

# Students

# Extracting data for students

X_Student = df.loc[df.Student == 1, 'Balance'].values.reshape(-1, 1)

y_Student = df.loc[df.Student == 1, 'Default']

# Creating a logistic regression model for students

log_reg_Student = LogisticRegression(solver='newton-cg')

_ = log_reg_Student.fit(X_Student, y_Student)

# Generating test data

X_gen = np.arange(df['Balance'].min(), df['Balance'].max()).reshape(-1, 1)

# Predicting probabilities for non-students and students

predicted_proba_NotStudent = log_reg_NotStudent.predict_proba(X_gen)

predicted_proba_Student = log_reg_Student.predict_proba(X_gen)

Group = Default.groupby(['Student','Default']).size().unstack('Default')

display(Group)

| Default | No | Yes |

|---|---|---|

| Student | ||

| No | 6850 | 206 |

| Yes | 2817 | 127 |

# Create subplots

fig, ax = plt.subplots(1, 2, figsize=(9, 4.5),gridspec_kw = {'width_ratios':[.75,.25]})

# Plot default probabilities for Non-Students and Students

_ = ax[0].plot(X_gen, predicted_proba_NotStudent[:, 1], color=CP['No'], label='Non-Student', lw = 1.5)

_ = ax[0].plot(X_gen, predicted_proba_Student[:, 1], color=CP['Yes'], label='Student', lw = 1.5)

Temp = ax[0].get_xlim()

# Plot dashed lines for overall default rates

_ = ax[0].hlines(Group.loc['Yes', 'Yes'] / Group.loc['Yes', 'No'], color=CP['Yes'],

lw = 1.5, label='Overall Student', xmin=Temp[0], xmax=Temp[1], linestyles='dashed')

_ = ax[0].hlines(Group.loc['No', 'Yes'] / Group.loc['No', 'No'],

lw = 1.5, color=CP['No'], label='Overall Non-Student', xmin=Temp[0], xmax=Temp[1], linestyles='dashed')

# Set common labels, ticks, and limits for the left plot

_ = ax[0].set(title='Default Probability vs. Credit Card Balance',

ylabel='Default Rate', xlabel='Credit Card Balance',

xlim = (X_gen.min(), X_gen.max()),

yticks = list(np.round(np.linspace(0, 1, 6), 1))

)

_ = ax[0].legend(loc=2)

_ = ax[0].grid(False)

# Create a boxplot for Student vs. Non-Student balance

_ = sns.boxplot(x='Student', y='Balance', data=Default, orient='v', ax=ax[1], palette=CP)

# Set common labels and title for the right plot

_ = ax[1].set(title='Credit Card Balance Distribution for\nStudent vs. Non-Student',

xlabel='Student', ylabel='Credit Card Balance')

# Adjust layout and display the plots

plt.tight_layout()

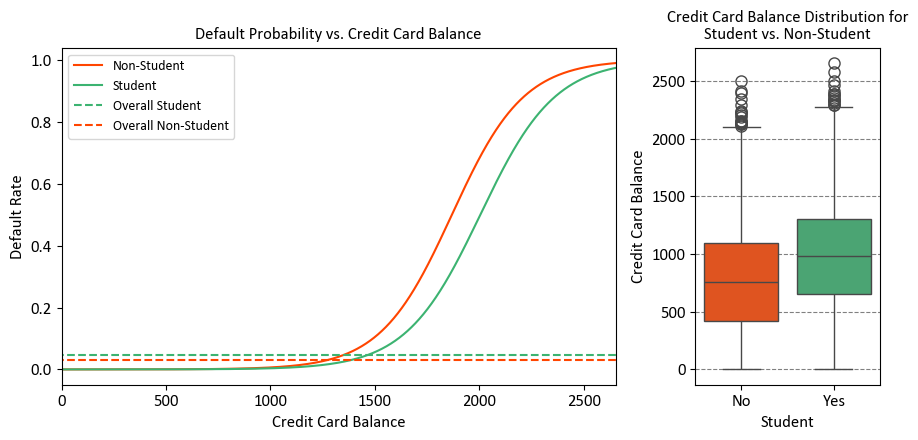

The right-hand panel of the figure provides a clear explanation for the observed disparity. It’s evident that the variables “student” and “balance” exhibit a correlation. Typically, students maintain higher levels of debt, and this higher indebtedness is associated with an elevated likelihood of default. In essence, students tend to carry larger credit card balances, a fact we glean from the left-hand panel of the figure, which also shows that substantial credit card balances are linked to elevated default rates.

Even though an individual student with a specific credit card balance would generally have a lower default probability compared to a non-student with the same balance, the aggregate behavior emerges due to students, on average, maintaining larger credit card balances. Consequently, when considering the overall scenario, students exhibit a higher default rate than non-students. This distinction is pivotal, especially for a credit card company aiming to make informed decisions about extending credit.

The level of risk associated with a student surpasses that of a non-student when no information about the student’s credit card balance is available. However, when comparing a student to a non-student with an equivalent credit card balance, the student is actually less risky.

Visual representation: The left-hand panel illustrates default rates for students (orange) and non-students (green). The solid lines depict the default rate based on the balance, while the horizontal broken lines indicate the overall default rates. In the right-hand panel, we see boxplots representing the distribution of balance for students (orange) and non-students (green).

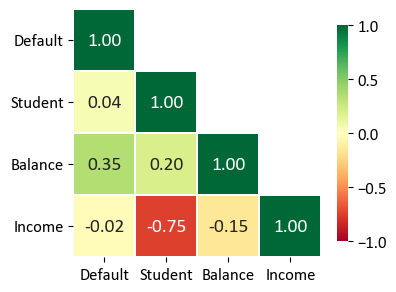

display(df.corr().style.background_gradient(cmap='RdYlGn', vmin= -1, vmax= 1).format(precision=2))

def Correlation_Plot (Df,Fig_Size):

Correlation_Matrix = Df.corr().round(2)

mask = np.zeros_like(Correlation_Matrix)

mask[np.triu_indices_from(mask)] = True

for i in range(len(mask)):

mask[i,i]=0

fig, ax = plt.subplots(figsize=(Fig_Size,Fig_Size))

sns.heatmap(Correlation_Matrix, ax=ax, mask=mask, annot=True, square=True,

fmt='.2f', cmap = 'RdYlGn',

linewidths = 0.2, vmin=-1, vmax=1,

annot_kws={"size": 14}, cbar_kws={"shrink": .7})

ax.set_yticklabels(ax.get_yticklabels(), rotation=0)

ax.grid(False)

Correlation_Plot (df, 4)

| Default | Student | Balance | Income | |

|---|---|---|---|---|

| Default | 1.00 | 0.04 | 0.35 | -0.02 |

| Student | 0.04 | 1.00 | 0.20 | -0.75 |

| Balance | 0.35 | 0.20 | 1.00 | -0.15 |

| Income | -0.02 | -0.75 | -0.15 | 1.00 |

The table you provided is a correlation matrix that shows the pairwise correlations between different variables in the dataset. Each value in the table represents the correlation coefficient between two variables. The correlation coefficient measures the strength and direction of the linear relationship between two variables:

Default and Student: The correlation coefficient is 0.04. This indicates a very weak positive correlation between being a student and defaulting on payments. In other words, being a student has a very slight tendency to be associated with a slightly higher probability of defaulting.

Default and Balance: The correlation coefficient is 0.35. This value indicates a moderate positive correlation between credit card balance and default. A higher credit card balance is associated with a moderately higher probability of defaulting.

Default and Income: The correlation coefficient is -0.02. This indicates a very weak negative correlation between income and default. There’s almost no noticeable linear relationship between income and the probability of defaulting.

Student and Balance: The correlation coefficient is 0.20. This shows a weak positive correlation between being a student and credit card balance. Being a student is somewhat associated with having a slightly higher credit card balance.

Student and Income: The correlation coefficient is -0.75. This indicates a strong negative correlation between being a student and income. Being a student is significantly associated with having lower income.

Balance and Income: The correlation coefficient is -0.15. This represents a weak negative correlation between credit card balance and income. Individuals with higher credit card balances tend to have slightly lower incomes.

In summary, the correlation matrix provides insights into the relationships between different variables. Positive correlation values indicate that as one variable increases, the other tends to increase as well. Negative correlation values suggest that as one variable increases, the other tends to decrease. The magnitude of the correlation coefficient indicates the strength of the relationship, with values closer to 1 or -1 indicating a stronger correlation. However, correlation does not imply causation, and other factors may contribute to these relationships.

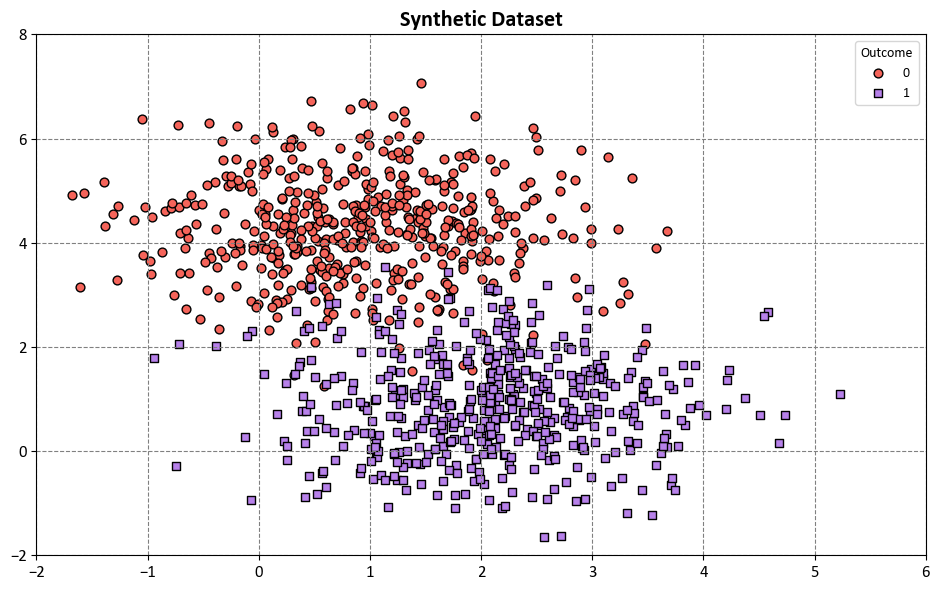

9.4.6. Example: Synthetic Dataset#

Example: In this code example, a Decision Tree Classifier is utilized to illustrate decision boundaries on synthetic data. The synthetic dataset is generated using the make_blobs function from scikit-learn, designed for creating artificial datasets for various machine learning experiments. This particular dataset consists of the following characteristics:

Number of Samples: 1000

Number of Features: 2

Number of Classes: 2

Random Seed (random_state): 0

Cluster Standard Deviation (cluster_std): 1.0

Features:

The dataset contains 1000 data points, each described by a pair of feature values. These features are represented as ‘Feature 1’ and ‘Feature 2’.

Outcome (Target Variable):

The dataset also includes a target variable called ‘Outcome.’ This variable assigns each data point to one of two distinct classes, identified as ‘Class 0’ and ‘Class 1’.

The dataset has been designed to simulate a scenario with two well-separated clusters, making it suitable for binary classification tasks. Each data point in this dataset is associated with one of the two classes, and it can be used for practicing and evaluating machine learning algorithms that deal with binary classification problems.

from sklearn.datasets import make_blobs

import seaborn as sns

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

# Generate synthetic data

X, y = make_blobs(n_samples=1000, centers=2, random_state=0, cluster_std=1.0)

# Create a scatter plot using Seaborn

fig, ax = plt.subplots(1, 1, figsize=(9.5, 6))

colors = ["#f5645a", "#b781ea"]

markers = ['o', 's']

# Scatter plot of data points

for num in np.unique(y):

ax.scatter(X[:, 0][y == num], X[:, 1][y == num], c=colors[num],

s=40, edgecolors="k", marker=markers[num], label=str(num))

ax.set(xlim=[-2, 6], ylim=[-2, 8])

ax.legend(title = 'Outcome')

ax.set_title('Synthetic Dataset', weight = 'bold', fontsize = 16)

plt.tight_layout()

The synthetic dataset depicted above exhibits a balanced distribution between two classes.

import seaborn as sns

import matplotlib.pyplot as plt

import numpy as np

fig, ax = plt.subplots(figsize=(5, 2))

_ = sns.countplot(y = y, palette= colors, ec = 'k')

_ = ax.set(xlabel = 'Count', ylabel = 'Outcome' )

plt.tight_layout()

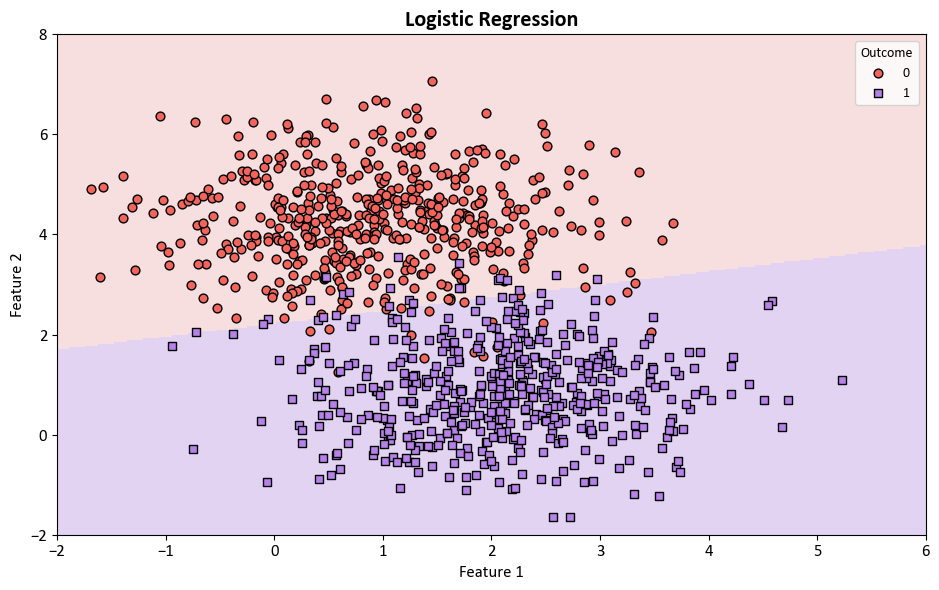

Next, Logistic Regression from the scikit-learn library [scikit-learn Developers, 2023] is employed for the classification of the aforementioned dataset.

from sklearn.linear_model import LogisticRegression

from matplotlib.colors import ListedColormap

from sklearn.inspection import DecisionBoundaryDisplay

colors = ["#f5645a", "#b781ea"]

edge_colors = ['#8A0002', '#3C1F8B']

cmap_light = ListedColormap(['#f7dfdf', '#e3d3f2'])

markers = ['o', 's']

# Plot decision boundaries

fig, ax = plt.subplots(1, 1, figsize=(9.5, 6))

log_reg = LogisticRegression(max_iter = 200, solver = 'lbfgs')

log_reg.fit(X, y)

DecisionBoundaryDisplay.from_estimator(log_reg, X, cmap=cmap_light, ax=ax,

response_method="predict",

plot_method="pcolormesh",

xlabel= 'Feature 1', ylabel='Feature 2',

shading="auto", grid_resolution = 300)

# Scatter plot of data points

for num in np.unique(y):

ax.scatter(X[:, 0][y == num], X[:, 1][y == num], c=colors[num],

s=40, edgecolors="k", marker=markers[num], label=str(num))

ax.set(xlim=[-2, 6], ylim=[-2, 8])

ax.legend(title = 'Outcome')

ax.set(xlim=[-2, 6], ylim=[-2, 8])

ax.set_title(f'Logistic Regression', fontweight='bold', fontsize = 16)

ax.grid(False)

plt.tight_layout()

In practical application, it is imperative to take into account the division of the dataset into two distinct subsets: one designated for model training and the other for model testing. This separation can be achieved using the train_test_split function, as exemplified below:

import pandas as pd

import numpy as np

from sklearn.model_selection import train_test_split

from sklearn.linear_model import LogisticRegression

from sklearn.metrics import classification_report

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size= 0.25, random_state=0)

print(f'Shape of X_train = {X_train.shape}')

print(f'Shape of y_train = {y_train.shape}')

print(f'Shape of X_test = {X_test.shape}')

print(f'Shape of y_test = {y_test.shape}')

log_reg = LogisticRegression()

_ = log_reg.fit(X_train, y_train)

def _gen_cr(model, X, y):

y_pred = model.predict(X)

Results = pd.DataFrame(classification_report(y, y_pred,

output_dict=True)).T

display(Results.style.format(precision = 3))

print('\nTrain Data:')

_gen_cr(log_reg, X_train, y_train)

print('\nTest Data:')

_gen_cr(log_reg, X_test, y_test)

Shape of X_train = (750, 2)

Shape of y_train = (750,)

Shape of X_test = (250, 2)

Shape of y_test = (250,)

Train Data:

| precision | recall | f1-score | support | |

|---|---|---|---|---|

| 0 | 0.965 | 0.965 | 0.965 | 372.000 |

| 1 | 0.966 | 0.966 | 0.966 | 378.000 |

| accuracy | 0.965 | 0.965 | 0.965 | 0.965 |

| macro avg | 0.965 | 0.965 | 0.965 | 750.000 |

| weighted avg | 0.965 | 0.965 | 0.965 | 750.000 |

Test Data:

| precision | recall | f1-score | support | |

|---|---|---|---|---|

| 0 | 0.952 | 0.938 | 0.945 | 128.000 |

| 1 | 0.935 | 0.951 | 0.943 | 122.000 |

| accuracy | 0.944 | 0.944 | 0.944 | 0.944 |

| macro avg | 0.944 | 0.944 | 0.944 | 250.000 |

| weighted avg | 0.944 | 0.944 | 0.944 | 250.000 |

Remark

The classification_report function in scikit-learn is a powerful tool for generating a comprehensive report that evaluates the performance of a classification model. It provides a breakdown of various metrics such as precision, recall, F1-score, and support for each class in the classification problem. This report helps you understand how well the model is performing for different classes and allows you to make informed decisions about its performance [Pedregosa et al., 2011, scikit-learn Developers, 2023].

classification_report(y_true, y_pred, target_names=None, sample_weight=None, digits=2, output_dict=False)

y_true: The true target values for the test set.y_pred: The predicted target values for the test set.target_names: A list of class names. If provided, it helps label the rows of the report.sample_weight: Optional weights that can be assigned to individual samples.digits: The number of decimal places for displaying the results.output_dict: If True, the function returns the classification report as a dictionary.

The output of classification_report is a nicely formatted string (if output_dict is False) or a dictionary (if output_dict is True) containing precision, recall, F1-score, and support metrics for each class. The metrics are calculated based on the true and predicted labels.

For example, if you have a binary classification problem with classes “Positive” and “Negative,” the report might look like this:

precision recall f1-score support

Positive 0.80 0.90 0.85 100

Negative 0.70 0.50 0.58 50

accuracy 0.77 150

macro avg 0.75 0.70 0.71 150

weighted avg 0.76 0.77 0.76 150

Precision: The ability of the model to correctly identify positive instances among the instances it labeled as positive.

Recall: The ability of the model to correctly identify all positive instances among all actual positive instances.

F1-score: The harmonic mean of precision and recall. It balances precision and recall and is useful when classes are imbalanced.

Support: The number of actual occurrences of the class in the test set.

The performance of the trained model on both the training and testing datasets is as follows:

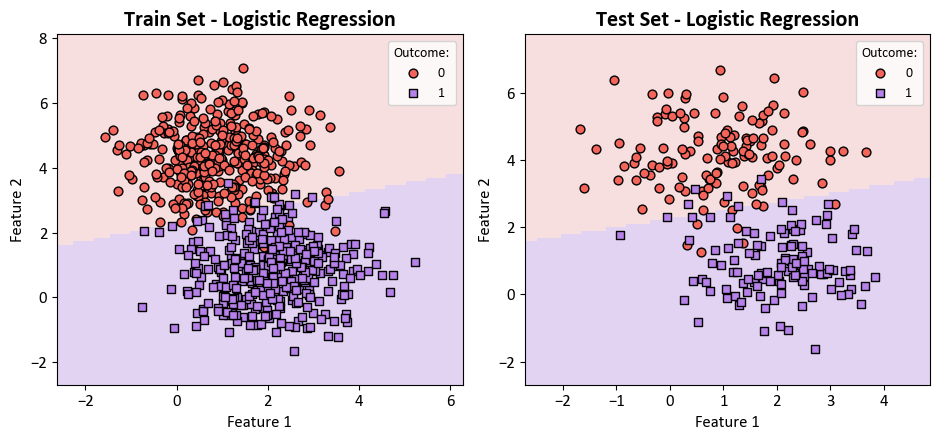

from matplotlib.colors import ListedColormap

from sklearn.inspection import DecisionBoundaryDisplay

fig, axes = plt.subplots(1, 2, figsize=(9.5, 4.5))

# Create a loop for train and test sets

for i, (X_set, y_set, title) in enumerate([(X_train, y_train, 'Train Set'), (X_test, y_test, 'Test Set')]):

# Plot decision boundaries

DecisionBoundaryDisplay.from_estimator(log_reg, X_set, cmap=cmap_light, ax=axes[i],

response_method="predict",

plot_method="pcolormesh",

xlabel='Feature 1', ylabel='Feature 2',

shading="auto")

for num in np.unique(y):

axes[i].scatter(X_set[:, 0][y_set == num],

X_set[:, 1][y_set == num], c=colors[num],

s=40, edgecolors="k", marker=markers[num], label=str(num))

axes[i].legend(title = 'Outcome:')

axes[i].set_title(f'{title} - Logistic Regression', fontweight='bold', fontsize=16)

axes[i].grid(False)

plt.tight_layout()

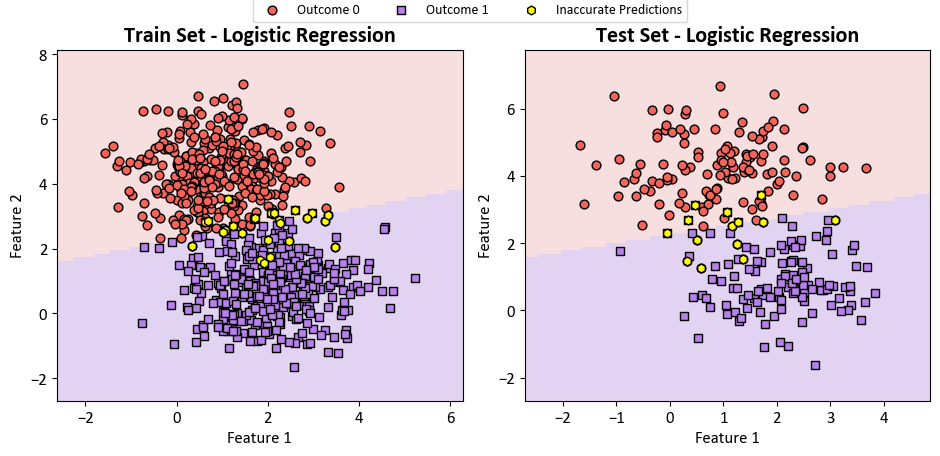

Upon closer examination, it becomes evident that certain data points from the set X have been misclassified. These instances are visually highlighted with yellow circles in the subsequent figure.

from matplotlib.colors import ListedColormap

from sklearn.inspection import DecisionBoundaryDisplay

fig, axes = plt.subplots(1, 2, figsize=(9.5, 4.5))

# Create a loop for train and test sets

for i, (X_set, y_set, title) in enumerate([(X_train, y_train, 'Train Set'), (X_test, y_test, 'Test Set')]):

# Plot decision boundaries

DecisionBoundaryDisplay.from_estimator(log_reg, X_set, cmap=cmap_light, ax=axes[i],

response_method="predict",

plot_method="pcolormesh",

xlabel='Feature 1', ylabel='Feature 2',

shading="auto")

for num in np.unique(y):

axes[i].scatter(X_set[:, 0][y_set == num],

X_set[:, 1][y_set == num], c=colors[num],

s=40, edgecolors="k", marker=markers[num], label= f'Outcome {num}')

# Plot data points where y_set and log_reg(X_set) differ in color

axes[i].scatter(X_set[:, 0][y_set != log_reg.predict(X_set)],

X_set[:, 1][y_set != log_reg.predict(X_set)],

fc='Yellow', ec='black', s=40, marker= 'h', label= 'Inaccurate Predictions')

axes[i].set_title(f'{title} - Logistic Regression', fontweight='bold', fontsize=16)

axes[i].grid(False)

# Remove the legend for each panel

axes[i].legend()

axes[i].get_legend().remove()

# Create a single legend for both subplots at the top

handles, labels = axes[0].get_legend_handles_labels()

fig.legend(handles, labels, loc='upper center', ncol=3, borderaxespad= -0.1)

plt.tight_layout()

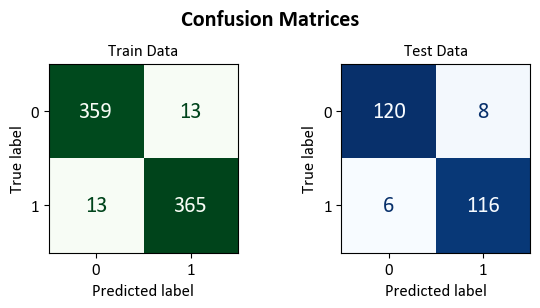

Lastly, we present the confusion matrix below:

import matplotlib.pyplot as plt # Import matplotlib for plotting

from sklearn.metrics import ConfusionMatrixDisplay, confusion_matrix # Import necessary functions/classes

def format_confusion_matrix(cm, title):

true_neg, false_pos, false_neg, true_pos = cm.ravel()

result = f"\033[1m{title} Set Confusion Matrix\033[0m:\n"

result += f"- {true_neg} instances were correctly predicted as class 0.\n"

result += f"- {true_pos} instances were correctly predicted as class 1.\n"

result += f"- {false_pos} instance was incorrectly predicted as class 1 when it was actually class 0.\n"

result += f"- {false_neg} instances were incorrectly predicted as class 0 when they were actually class 1.\n"

return result

def plot_cm(model, X_train, X_test, y_train, y_test, class_names, figsize=(7, 4)):

# Create a figure and axes for displaying confusion matrices side by side

fig, ax = plt.subplots(1, 2, figsize=figsize)

datasets = [(X_train, y_train, 'Train'), (X_test, y_test, 'Test')]

for i in range(2):

X, y, dataset_name = datasets[i]

# Compute confusion matrix for the dataset predictions

cm = confusion_matrix(y, model.predict(X))

result = format_confusion_matrix(cm, dataset_name)

print(result)

# Create a ConfusionMatrixDisplay and plot it on the respective axis

cm_display = ConfusionMatrixDisplay(cm, display_labels=class_names)\

.plot(ax=ax[i],

im_kw=dict(cmap='Greens' if dataset_name == 'Train' else 'Blues'),

text_kw={"size": 16}, colorbar=False)

ax[i].set_title(f'{dataset_name} Data')

ax[i].grid(False)

# Add a super title for the entire figure

fig.suptitle('Confusion Matrices', fontsize=16, weight = 'bold')

# Adjust the layout for better spacing

plt.tight_layout()

plot_cm(log_reg, X_train, X_test, y_train, y_test, ['0', '1'], figsize=(6, 3))

Train Set Confusion Matrix:

- 359 instances were correctly predicted as class 0.

- 365 instances were correctly predicted as class 1.

- 13 instance was incorrectly predicted as class 1 when it was actually class 0.

- 13 instances were incorrectly predicted as class 0 when they were actually class 1.

Test Set Confusion Matrix:

- 120 instances were correctly predicted as class 0.

- 116 instances were correctly predicted as class 1.

- 8 instance was incorrectly predicted as class 1 when it was actually class 0.

- 6 instances were incorrectly predicted as class 0 when they were actually class 1.

9.4.7. Multiclass Classifier#

A multiclass classifier is a model capable of predicting one of more than two possible classes for a given input. For instance, a multiclass classifier could identify the color of a flower as red, blue, or green, or classify an animal as a dog, cat, or bird.

However, not all classification models are inherently equipped to handle multiclass problems. Many linear models are designed for binary classification, which involves only two possible classes, such as yes or no, positive or negative, and so on.

To extend a binary classification model to a multiclass classification model, various techniques can be employed. One of the most common ones is the one-vs.-rest (OvR) approach, also known as one-vs.-all (OvA) or binary relevance (BR).

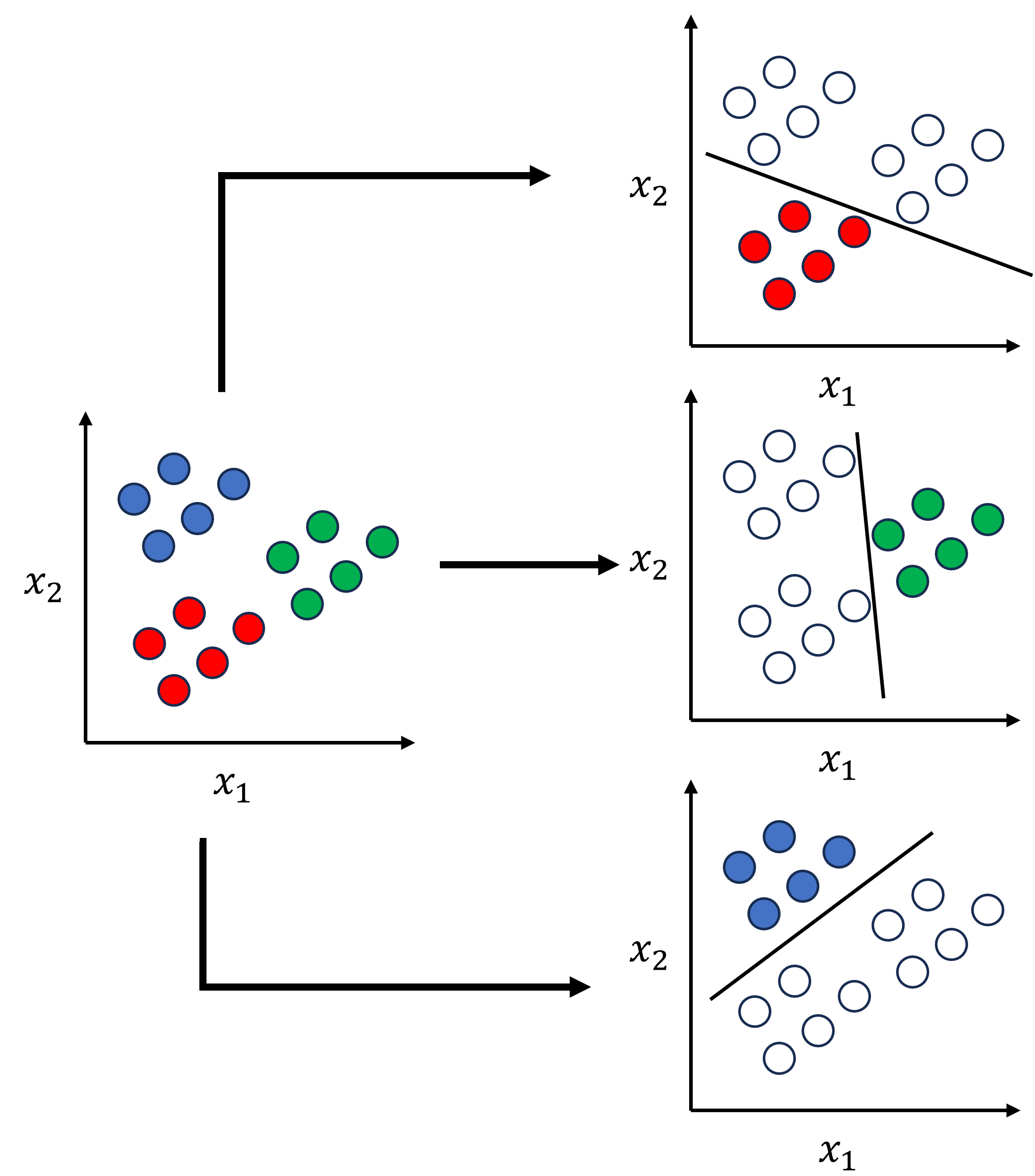

9.4.7.1. One-vs.-Rest Approach#

The OvR approach is a simple and intuitive way to use binary classifiers for multiclass classification. The idea is to train one binary classifier for each class, where the target class is treated as positive and the rest of the classes are treated as negative.

For example, if you have three classes, R, G, and B, you can create three binary classifiers:

Classifier 1: R vs (B or G)

Classifier 2: G vs (R or B)

Classifier 3: B vs (R or G)

Fig. 9.5 Example for One-vs.-Rest Approach.#

Each classifier will output a probability of belonging to its positive class, such as R, G, and B. Then, you can compare the probabilities and choose the class with the highest probability as the final prediction.

The OvR approach has several advantages, such as simplicity, speed, and ease of implementation. However, it also has some drawbacks:

It may encounter class imbalance, as the negative class is typically much larger than the positive class. This imbalance may affect the performance and accuracy of the classifiers.

It assumes that the classes are mutually exclusive, meaning that an input can only belong to one class. However, this assumption may not hold true for some problems, such as multi-label classification, where an input can belong to multiple classes.

It does not account for correlations or dependencies between the classes, which may impact the quality of the predictions.

9.4.7.2. Multinomial Logistic Regression#

Multinomial logistic regression is a model that can handle multiple classes directly, unlike binary logistic regression that can only handle two classes. It is an extension of binary logistic regression that creates a binary model for each class and then combines them using a softmax function. The softmax function is a mathematical function that turns a vector of numbers into a vector of probabilities that add up to one. It gives each class a probability, and the class with the highest probability is the most likely one. The model can be expressed as [James et al., 2023]:

Multiclass logistic regression offers several benefits:

It is more accurate and flexible, as it can reflect the true patterns and relationships in the data.

It avoids the problems of class imbalance or mutual exclusivity, as it assigns a probability to each class independently.

It can handle both ordinal and nominal classes, meaning that the classes can either have an order or not.

However, multinomial logistic regression also has some limitations:

It may be more costly and complex, as it requires more parameters and computations than binary logistic regression.

It may be more susceptible to the effects of regularization, a method used to prevent overfitting or underfitting. Regularization works by adding a penalty term to the cost function that depends on the size or complexity of the model parameters. The amount of regularization needs to be carefully chosen to balance the bias and variance of the model.

9.4.7.3. Sklearn Logistic Regression#

Sklearn is a popular Python library for machine learning and data science. Sklearn provides a logistic regression model that can handle both binary and multiclass classification problems. Sklearn logistic regression allows us to use either the OvR or the multinomial approach by setting the multi_class hyperparameter to either 'ovr' or 'multinomial', respectively. The default value is 'auto', which means that the algorithm will choose the best option based on the data and the solver [scikit-learn Developers, 2023].

The multi_class hyperparameter is different from the class_weight hyperparameter, which is used to adjust the weights of the classes to account for class imbalance. The class_weight hyperparameter can be set to either 'balanced' or a dictionary of class weights [scikit-learn Developers, 2023].

You can find more information and examples about sklearn logistic regression and the multi_class and class_weight hyperparameters in the documentation and this tutorial [scikit-learn Developers, 2023].

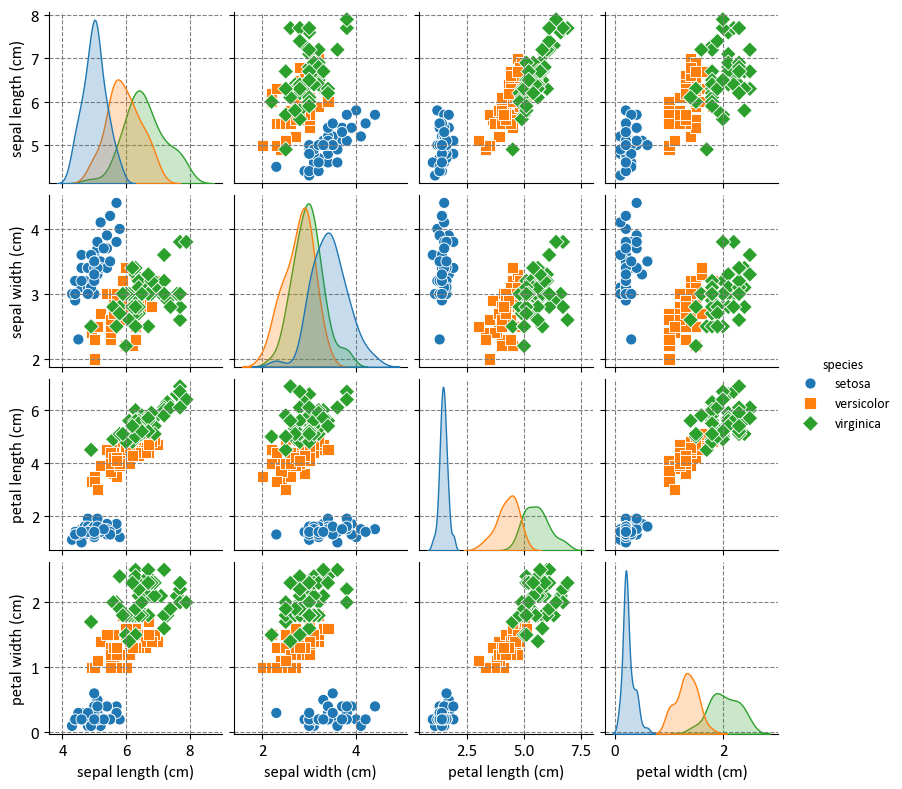

Example: The Iris Dataset serves as a quintessential example in explaining cross-validations. Crafted by the eminent British biologist and statistician Ronald A. Fisher in 1936, the dataset finds its roots in the realm of discriminant analysis. Named after the Iris flower species it encapsulates, this dataset stands as a foundational cornerstone in machine learning and statistics.

Dataset Composition

This dataset encompasses measurements of four distinct attributes in three diverse species of Iris flowers:

Sepal Length

Sepal Width

Petal Length

Petal Width

The dataset encapsulates three distinct species of Iris flowers:

Iris setosa

Iris versicolor

Iris virginica

Each Iris flower species is accompanied by precisely 50 samples, culminating in a total dataset size of 150 instances.

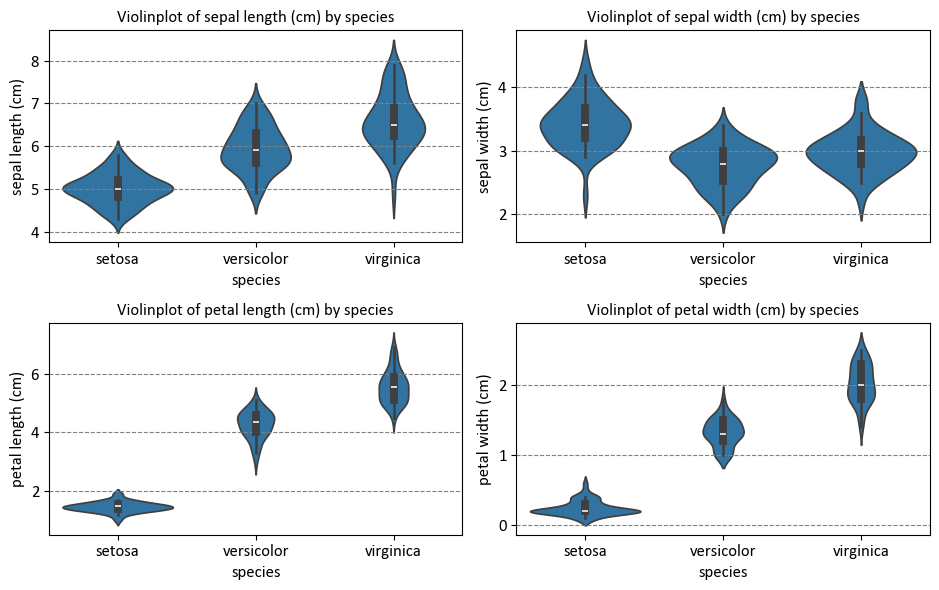

Before delving into that, let’s first examine the distribution of the dataset:

import warnings

warnings.simplefilter(action='ignore')

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from sklearn.datasets import load_iris

plt.style.use('../mystyle.mplstyle')

# Load the Iris dataset

iris = load_iris()

# Create a Pandas DataFrame

iris_df = pd.DataFrame(data=iris.data, columns= iris.feature_names)

iris_df['species'] = iris.target_names[iris.target]

# Print the first few rows of the DataFrame

display(iris_df.head())

# Pairplot: Scatterplots for each pair of features

g = sns.pairplot(iris_df, hue="species", markers=["o", "s", "D"], height = 2)

# _ = g.map_lower(sns.kdeplot, levels=4, color=".2")

# Create a 2x2 grid of subplots with a specified figure size

fig, ax = plt.subplots(2, 2, figsize=(9.5, 6))

# Flatten the 2x2 grid into a 1D array of subplots

ax = ax.ravel()

# Get the column names of the iris DataFrame, excluding the 'species' column

Cols = iris_df.drop(columns=['species']).columns

# Iterate through the columns using enumerate

for c, col in enumerate(Cols):

# Create a violin plot using Seaborn

sns.violinplot(x="species", y=col, data = iris_df, ax=ax[c])

# Set the title for the subplot

ax[c].set_title(f"Violinplot of {col} by species")

# Adjust the layout of the subplots for better visualization

plt.tight_layout()

| sepal length (cm) | sepal width (cm) | petal length (cm) | petal width (cm) | species | |

|---|---|---|---|---|---|

| 0 | 5.1 | 3.5 | 1.4 | 0.2 | setosa |

| 1 | 4.9 | 3.0 | 1.4 | 0.2 | setosa |

| 2 | 4.7 | 3.2 | 1.3 | 0.2 | setosa |

| 3 | 4.6 | 3.1 | 1.5 | 0.2 | setosa |

| 4 | 5.0 | 3.6 | 1.4 | 0.2 | setosa |

import matplotlib.pyplot as plt

import seaborn as sns

from matplotlib.colors import ListedColormap

from sklearn import datasets

from sklearn.linear_model import LogisticRegression

from sklearn.inspection import DecisionBoundaryDisplay

from sklearn.model_selection import train_test_split

from sklearn.metrics import classification_report

def print_bold(txt, c = 31):

print(f"\033[1;{c}m" + txt + "\033[0m")

# Load the Iris dataset

iris = datasets.load_iris()

# Select only the first two features for visualization

X = iris.data[:, :2]

y = iris.target

# Split the data into training and testing sets

X_train, X_test, y_train, y_test = train_test_split(X, y, test_size=0.2, random_state=42)

# Create color maps

colors = ["Red", "Blue", "Green"]

# Different values of multi_class

multi_class_values = ['ovr', 'multinomial']

# Create a 1x2 plot

fig, axes = plt.subplots(1, 2, figsize=(9.5, 4.5))

axes = axes.ravel()

for ax, multi_class in zip(axes, multi_class_values):

# Create a Logistic Regression classifier

lr = LogisticRegression(multi_class=multi_class, solver='lbfgs')

lr.fit(X_train, y_train)

# Evaluate the model

y_pred_train = lr.predict(X_train)

y_pred_test = lr.predict(X_test)

# Plot decision boundaries

display_dbd = DecisionBoundaryDisplay.from_estimator(lr, X_train, response_method="predict",

cmap= ListedColormap(colors),

alpha=0.1, ax=ax,

grid_resolution = 300)

# Plot training points

sns.scatterplot(x=X_train[:, 0], y=X_train[:, 1], hue=iris.target_names[y_train],

palette=colors, alpha=1.0, edgecolor="black", ax=ax)

# Set the title

_ = ax.set(xlabel=iris.feature_names[0],

ylabel=iris.feature_names[1])

_ = ax.set_title(f"Logistic Regression classification (multi_class = {multi_class})", weight = 'bold')

# Print the classification report

print_bold(f'{lr.__class__.__name__}: {multi_class}')

print_bold("\tTrain Classification Report:", 34)

display(pd.DataFrame(classification_report(y_train, y_pred_train, target_names=iris.target_names, output_dict=True)).T)

print_bold("\tTest Classification Report:", 34)

display(pd.DataFrame(classification_report(y_test, y_pred_test, target_names=iris.target_names, output_dict=True)).T)

ax.grid(False)

# Adjust the layout of the subplots for better visualization

plt.tight_layout()

LogisticRegression: ovr

Train Classification Report:

| precision | recall | f1-score | support | |

|---|---|---|---|---|

| setosa | 0.975000 | 0.975000 | 0.975000 | 40.000000 |

| versicolor | 0.666667 | 0.634146 | 0.650000 | 41.000000 |

| virginica | 0.658537 | 0.692308 | 0.675000 | 39.000000 |

| accuracy | 0.766667 | 0.766667 | 0.766667 | 0.766667 |

| macro avg | 0.766734 | 0.767151 | 0.766667 | 120.000000 |

| weighted avg | 0.766802 | 0.766667 | 0.766458 | 120.000000 |

Test Classification Report:

| precision | recall | f1-score | support | |

|---|---|---|---|---|

| setosa | 1.000000 | 1.000000 | 1.000000 | 10.000000 |

| versicolor | 1.000000 | 0.777778 | 0.875000 | 9.000000 |

| virginica | 0.846154 | 1.000000 | 0.916667 | 11.000000 |

| accuracy | 0.933333 | 0.933333 | 0.933333 | 0.933333 |

| macro avg | 0.948718 | 0.925926 | 0.930556 | 30.000000 |

| weighted avg | 0.943590 | 0.933333 | 0.931944 | 30.000000 |

LogisticRegression: multinomial

Train Classification Report:

| precision | recall | f1-score | support | |

|---|---|---|---|---|

| setosa | 1.000000 | 1.000000 | 1.000000 | 40.0 |

| versicolor | 0.697674 | 0.731707 | 0.714286 | 41.0 |

| virginica | 0.702703 | 0.666667 | 0.684211 | 39.0 |

| accuracy | 0.800000 | 0.800000 | 0.800000 | 0.8 |

| macro avg | 0.800126 | 0.799458 | 0.799499 | 120.0 |

| weighted avg | 0.800084 | 0.800000 | 0.799749 | 120.0 |

Test Classification Report:

| precision | recall | f1-score | support | |

|---|---|---|---|---|

| setosa | 1.000000 | 1.000000 | 1.000000 | 10.0 |

| versicolor | 0.875000 | 0.777778 | 0.823529 | 9.0 |

| virginica | 0.833333 | 0.909091 | 0.869565 | 11.0 |

| accuracy | 0.900000 | 0.900000 | 0.900000 | 0.9 |

| macro avg | 0.902778 | 0.895623 | 0.897698 | 30.0 |

| weighted avg | 0.901389 | 0.900000 | 0.899233 | 30.0 |

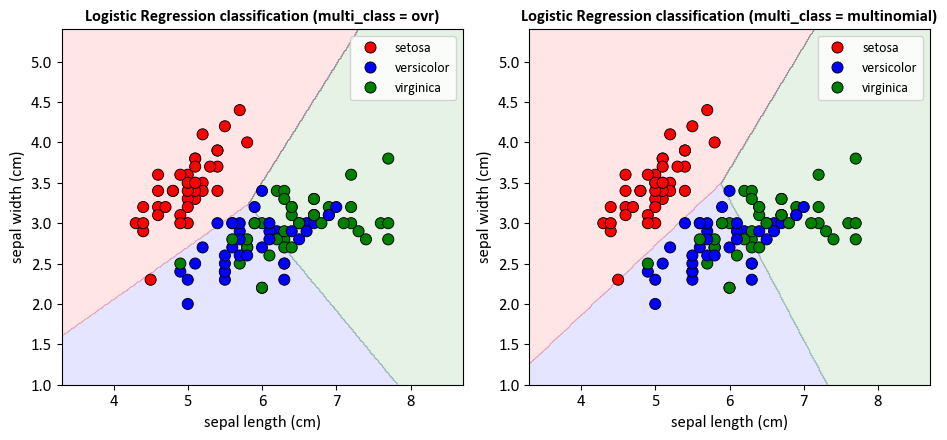

For the LogisticRegression model with multi_class='ovr':

The training set accuracy is approximately 0.77, and the testing set accuracy is approximately 0.93. This means that the model correctly classified 77% of the samples in the training set and 93% of the samples in the testing set.

The precision, recall, and F1-score for each class vary. For example, the model has perfect precision, recall, and F1-score for the ‘setosa’ class in the testing set.

For the LogisticRegression model with multi_class='multinomial':

The training set accuracy is approximately 0.80, and the testing set accuracy is approximately 0.90. This means that the model correctly classified 80% of the samples in the training set and 90% of the samples in the testing set.

The precision, recall, and F1-score for each class vary. For example, the model has perfect precision, recall, and F1-score for the ‘setosa’ class in the testing set.